Get Your Free 1st Issue

Your Homes Overseas Magazine!

Discover the best destinations, property tips, and lifestyle insights from around the world.

GET YOUR FREE MAGAZINE HERE!

Discover the best destinations, property tips, and lifestyle insights from around the world.

GET YOUR FREE MAGAZINE HERE!

About International Property Alerts

International Property Alerts is a premier global platform connecting real estate investors with handpicked opportunities in emerging and lifestyle-driven markets. Through curated listings, expert guidance, and market insights, we help buyers make confident property decisions worldwide.

Media Contact:

![]()

Phone: +4420 3627 0106

📱 WhatsApp: +63927 073 9530

Email: office@internationalpropertyalerts.com

Elle Resort & Beach Club offers a rare chance to own property in one of the most desirable coastal locations. With limited units, strong capital growth potential, and unmatched resort facilities, this is your opportunity to secure a beachfront lifestyle with long-term value.

Thinking about buying property abroad? Don’t make the move without the right knowledge. Our Free Buyers Guide gives you essential insights on legal steps, taxes, financing, and the best markets worldwide. Trusted by international buyers and investors.

Wake up to bright, spacious living with stunning views and modern comforts. Whether for family living, retirement, or a stylish retreat, Sudara Residences makes your dream home a reality

Discover curated property listings with IPS—residential, commercial, villas, land—and get expert guidance through every step.

BONUS: FREE Cambodia Buyer’s Guide

High visibility. Targeted audience. Maximum exposure. Rent this space and let your brand shine.

Get your properties in front of high-intent investors. Showcase your listings to buyers worldwide.

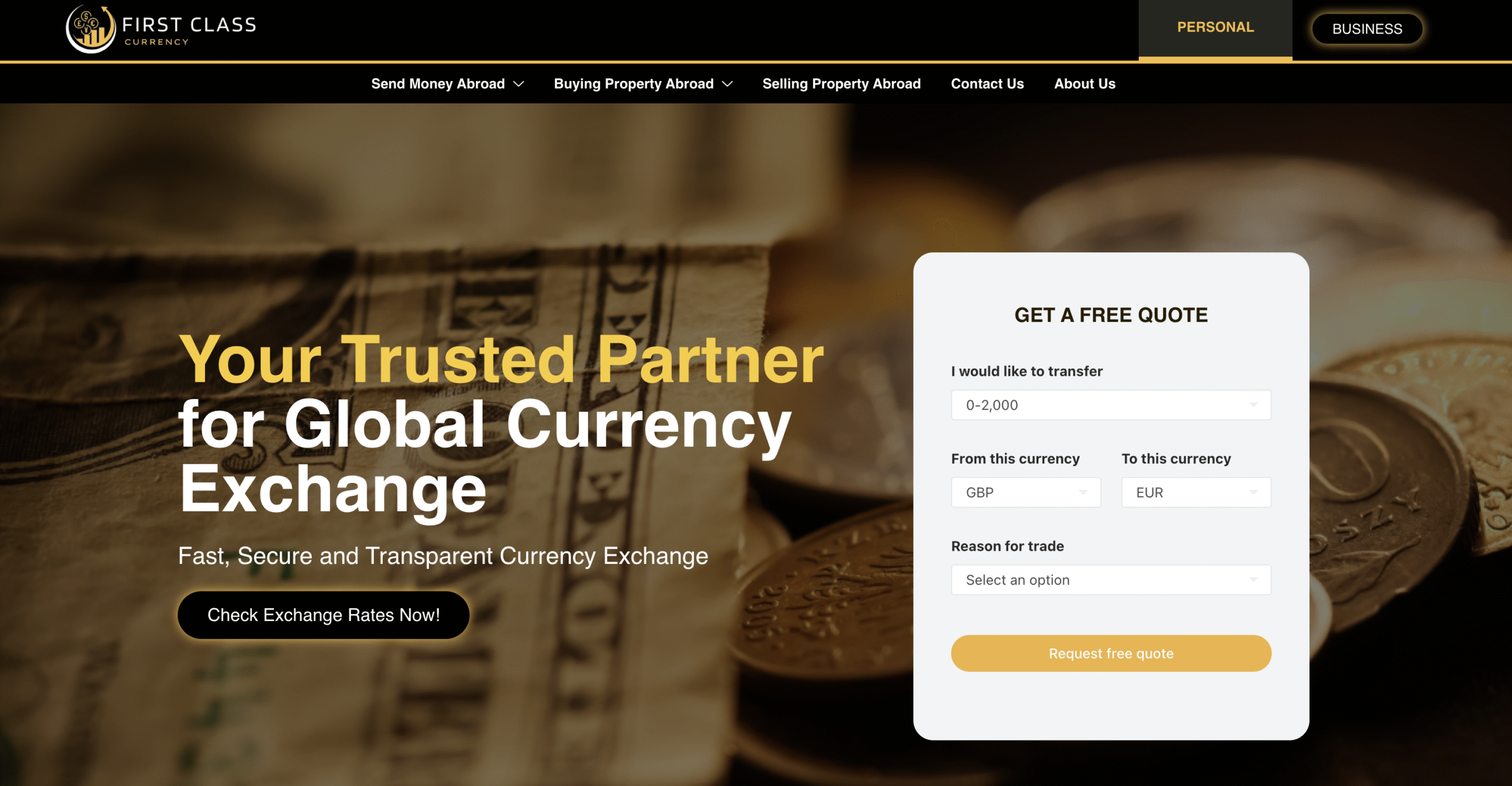

From pounds to pesos, yen to dollars. ⚡ Quick. Easy. Secure.

Compare listings

Compare